Why 72 Month Loans Are Crazy

I almost signed the papers on a 60-month truck loan fifteen years ago. The salesman leaned in with that fake-friendly grin and said, “Only $612 a month, Mr. Forge. You can swing that easy.” On paper it looked harmless. My income was climbing. I wanted the big diesel with the chrome package. But something in my gut screamed stop. I walked out, paid cash for a used ¾-ton with 80k miles, and never looked back. That single decision saved me tens of thousands and kept my cash flow free. Today, 72-month loans are everywhere—and they’re pure financial poison.

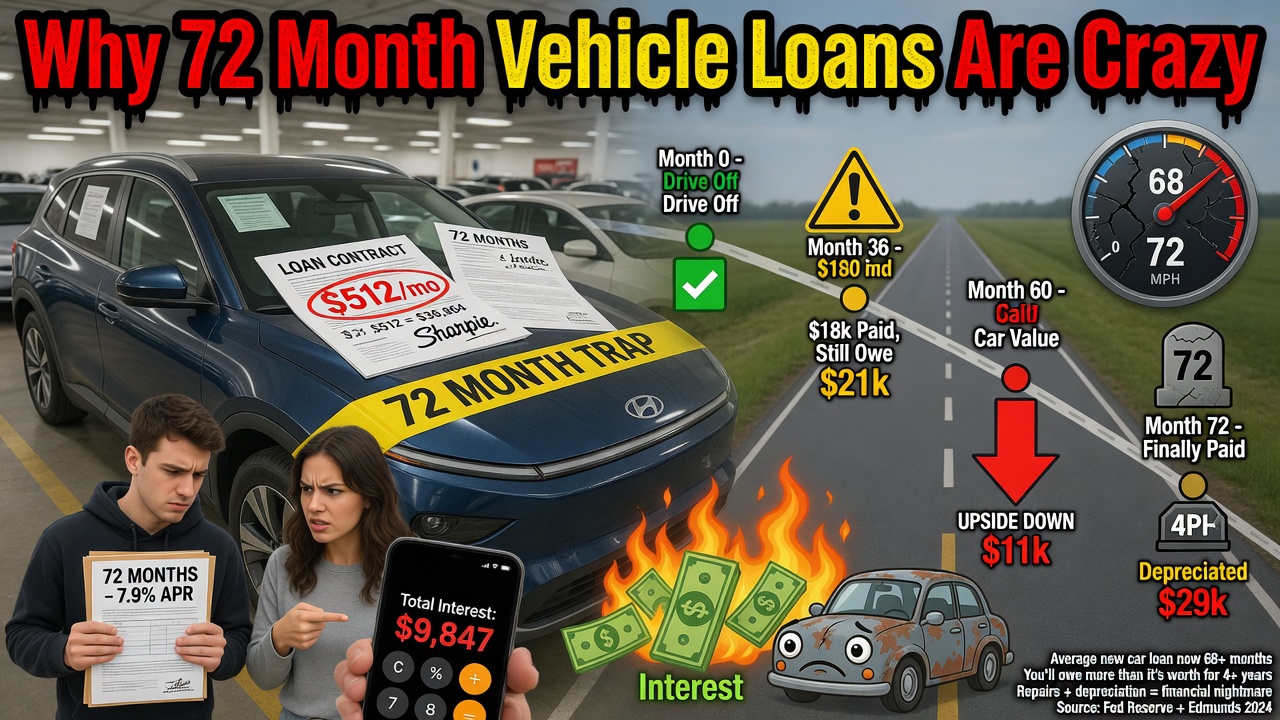

The Brutal Math That Proves 72 Months Is Financial Suicide

Let’s kill the fantasy with real numbers. Say you’re eyeing a $45,000 truck at 8% APR (the average rate I’m seeing in 2026 dealerships). Here’s what happens:

| Loan Term | Monthly Payment | Total Paid | Interest Paid | Real Cost Over 6 Years |

|---|---|---|---|---|

| 72 months | $789 | $56,808 | $11,808 | +26% of sticker price in interest |

| 36 months (what I recommend) | $1,410 | $50,760 | $5,760 | You own it outright in 3 years |

| Cash (no loan) | $0 | $45,000 | $0 | You keep the $11,808 + freedom |

That $11,808 in interest? It’s not “just the cost of financing.” That money could have been compounding in a boring index fund at 10% for the next decade and turned into over $30,000. But instead it vanished into a bank’s pocket while you drove a depreciating asset. That’s not a loan. That’s a wealth transfer disguised as “affordable payments.”

“Low monthly payments feel like freedom until you realize you’re chained to the payment for six damn years while the truck loses value every single month.”

The Psychology Trap: Why Your Brain Begs for 72-Month Loans

This is where the real damage happens—in your head. The salesman knows exactly what he’s doing. He sells you on the monthly number, not the total price. Your brain lights up because $789 feels doable. It feels like “balance.” You tell yourself you deserve the bigger truck after all those long hours. That’s the same hedonic treadmill I wrote about in The Psychology of Making Money. Comfort masquerading as balance is the silent killer of wealth.

I lived it. Early in business I let a 48-month lease sneak in because the payment fit my new income. Six months later I hated the truck, but I was upside-down by $9k. Lifestyle inflation had me by the throat. Every raise I got? Instantly absorbed by a nicer ride, bigger insurance, and that monthly anchor. Cash flow? Non-existent. Investments? Starved. I was making good money but still felt broke.

Pay the higher monthly now (or pay cash) and you own the asset free and clear. Skip it and you pay the tax forever—higher insurance, endless interest, and the constant psychological weight of debt.

How 72-Month Loans Murder Cash Flow (While Net Worth Looks Fine)

Cash flow beats net worth every single time. A shiny $45k truck on a 72-month loan shows up on your balance sheet as an “asset.” In reality it’s a $789/month liability that destroys your ability to invest, build emergency funds, or seize opportunities. I run my one-man empire on systems, not motivation. One of those systems is zero long-term auto debt. Because when cash flow is locked in payments, you can’t compound. You can’t buy the next boring business. You can’t weather the next oil shock or tariff-driven price spike.

I rewired my brain to crave hard work instead of comfort. Part of that was refusing the easy monthly payment. The 3 AM Rule helped: I was up at 3 a.m. three days a week running the numbers on every big purchase. The math never lied. Long loans always lost.

My 4-Step “72-Month Trap Avoidance Protocol” – Use It Today

- Run the real numbers. Always calculate total cost, not monthly. I keep a simple spreadsheet: sticker price + interest + insurance + fuel + maintenance for 72 months.

- Force the discipline tax. Whatever the 72-month payment is, I make myself pay double that amount in cash or on a 36-month max loan. If I can’t, I can’t afford the vehicle.

- Choose boring over exciting. A reliable 3-year-old truck that I can pay off in 24 months beats a brand-new status symbol every time. Boring beats exciting in cars just like in real estate and business.

- Build the cash-flow buffer first. I keep six months of all expenses (including car) in liquid cash before I ever sign anything. Debt feels different when you have options.

The Self-Made Man’s Code: Own Your Transportation, Don’t Lease Your Freedom

Capitalism rewards those who control their costs. Free markets gave us incredible trucks and cars, but predatory financing turned them into wealth shredders. Tariffs on imported steel and parts are raising prices right now—don’t compound that pain with a 72-month anchor. I still drive the same truck I bought cash years ago. It’s paid for, reliable, and every dollar I don’t send to the bank goes into my compounding machine.

Most people stay broke even when they make good money because they finance lifestyle instead of assets. Don’t be most people. Pay the discipline tax early. Rewire for hard work. Choose systems over motivation. And never, ever sign a 72-month loan.

The next time a salesman slides that contract across the desk and whispers “only $XXX a month,” remember this page. Walk out. Buy less car. Own it faster. Watch your cash flow explode and your real net worth finally move.

Pro-capitalism. Pro-tariffs. Pro-discipline. Pro-freedom.