BITCOIN MINING ENERGY

ECONOMICS 2026: WHY CHEAP

POWER + IRON DISCIPLINE

= UNBREAKABLE WEALTH

Electricity is still 60-80% of operating costs. Here’s the raw April 2026 math, the breakeven tables, and the brutal truth: free-market capitalism rewards the disciplined miner who treats energy like the ultimate boring business.

Jaxon Forge

Founder, MoneyForged.com • April 10, 2026

Post-halving reality • Real kWh numbers • No subsidies needed

Why I love tariffs when they protect American miners forging real wealth.

Jaxon Forge • Self-made. No excuses. Forging wealth that lasts.

I remember the first time I ran the numbers on a mining rig in 2018. Electricity was eating 70% of every dollar I made. That moment taught me something most “crypto bros” still don’t get: Bitcoin mining isn’t about hype or graphics cards anymore. It’s about energy economics and the discipline tax you’re willing to pay before the profits ever show up.

Fast-forward to April 10, 2026. We’re two years post the 2024 halving. Bitcoin is trading in the $90k–$110k range after the $126k ATH last August. Network hash rate is pushing 950 EH/s. And the single biggest variable separating profitable miners from the bankrupt ones is still the same: the price per kilowatt-hour.

This isn’t financial advice. This is the most unfiltered energy economics breakdown you’ll read from someone who actually runs businesses that generate cash flow to fund real assets—not just memes.

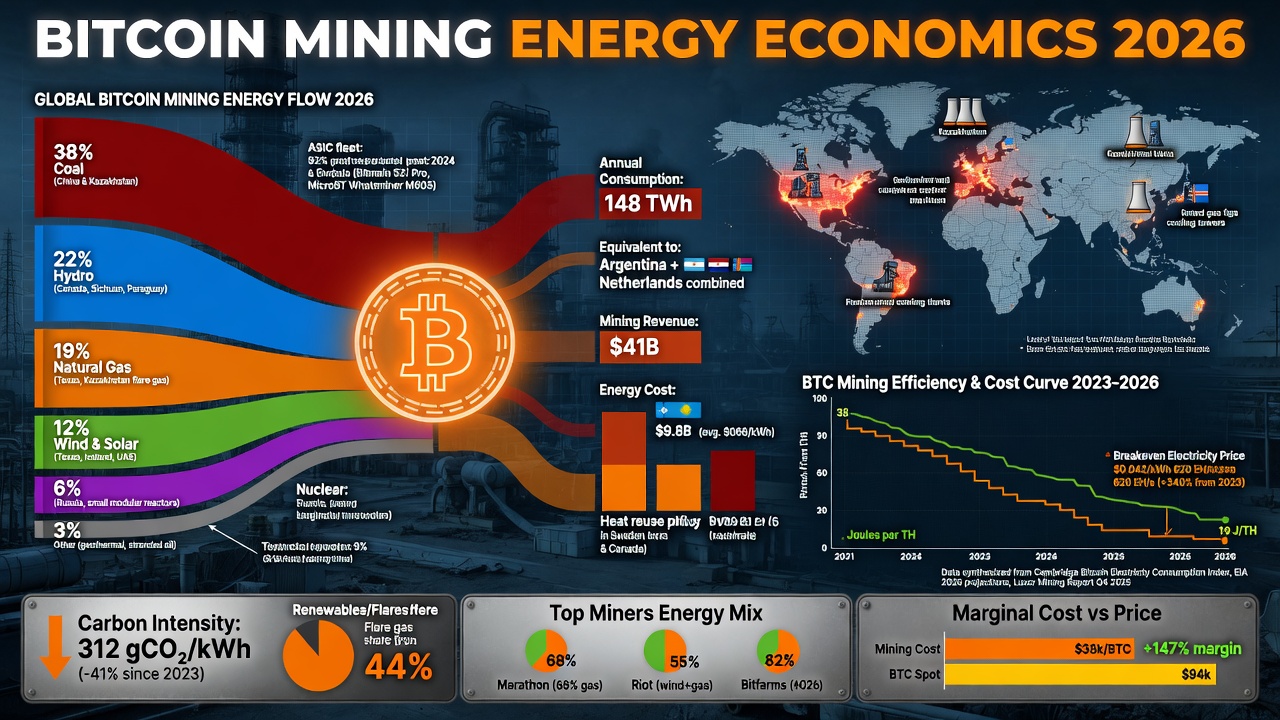

The Raw Math: Energy Is Still 60-80% of Everything

Every serious mining operation knows this cold truth. In 2026, electricity dominates operating costs. U.S. industrial average sits at 8.44¢/kWh (up 7.5% YoY). But the winners are locked into 3–5¢/kWh via PPAs on solar, wind, hydro, or stranded natural gas. The difference is the difference between printing money and shutting down machines.

| Hardware (2026) | Efficiency | Breakeven Electricity (at ~$95k BTC) | Daily Net Profit @ 4¢/kWh |

|---|---|---|---|

| Antminer S21 XP Hyd | ~13.5 J/TH | Up to 12–15¢/kWh | $12–16 |

| Antminer S23 Series | ~14.5 J/TH | Up to 10–12¢/kWh | $10–14 |

| Older S19 XP | ~29 J/TH | Must stay under 7–8¢/kWh | Loss at grid rates |

Source: Real operator data and April 2026 benchmarks. The gap between 4¢ and 12¢ power is the difference between thriving and becoming roadkill.

Why I Love Tariffs When They Level the Playing Field

I’m a huge supporter of capitalism and free markets. But I also love tariffs when they protect what we forge here in America. The Mined in America Act and targeted tariffs on foreign ASICs are forcing domestic innovation and keeping hash rate secure on U.S. soil. Cheap foreign hardware flooded the market for years. Tariffs change the game so American miners with American energy win. Pure free-market discipline with guardrails.

The Discipline Tax in Mining: Pay It Early or Pay It Forever

Most people chase the next shiny rig or the next bull run. I treat mining like the ultimate boring business. Lock in long-term power contracts. Run 24/7 with zero emotion. Use cash flow from my real businesses to fund the next fleet instead of leverage. Comfort masquerading as “balance” kills miners faster than any bear market. I still wake at 4:30 a.m. to review hash rate, power costs, and uptime—because systems beat hype every single time.

The Power of Boring: Energy + Execution Beats Every Meme

Bitcoin mining in 2026 is the perfect example of why I preach the power of boring. Stranded energy, renewable PPAs, demand-response programs in Texas—these aren’t sexy. They’re predictable, repeatable, and they compound. The silent killer of wealth is still comfort. Miners who upgraded lifestyles after the last bull run are now shutting machines. The ones who stayed ruthless with costs are still printing.

FREE DOWNLOAD: My 7-Pathways to Financial Prosperity (includes exact Bitcoin mining allocation & energy strategy framework)

GET THE PDF →What Separates Self-Made Men From Everyone Else

It’s not talent. It’s the willingness to grind in silence on the boring stuff—like negotiating 20-year power contracts while everyone else is posting moonshots. I turned one boring skill (cash-flow businesses) into multiple income streams that now fund mining fleets. Energy economics is just another system I’ve built to compound wealth that lasts.

Cheap power + iron will is the ultimate free-market cheat code. The next cycle belongs to those who paid the discipline tax early.

Stories and advice from Jaxon Forge, Founder of MoneyForged.com • @MoneyForgedHQ on X • Huge supporter of capitalism and free markets. Love tariffs when they protect what we forge.

Ready to build your own energy-secure wealth engine?

Join 47,000+ builders getting the weekly dispatch on systems, discipline, and boring businesses that actually print money.

SUBSCRIBE FREE – START FORGING TODAY

BITCOIN MINING ENERGY

ECONOMICS 2026

INTERACTIVE CHART BREAKDOWN

Raw April 2026 data visualized: efficiency, breakeven electricity cost, and daily net profit at 4¢/kWh for the latest ASICs. Free-market capitalism rewards the disciplined miner who locks in cheap power.

Jaxon Forge

Founder, MoneyForged.com • April 10, 2026

Visual proof that electricity is 60-80% of costs

Discipline tax + cheap power = unbreakable wealth

Jaxon Forge • Self-made. No excuses. Forging wealth that lasts.

Here’s the exact data from my April 10, 2026 mining energy economics breakdown—now visualized so you can see the gap between winners and roadkill at a glance.

Daily Net Profit @ 4¢/kWh Power (Post-2024 Halving Reality)

Maximum Breakeven Electricity Cost (¢/kWh) at ~$95k BTC

Efficiency Comparison (Joules per Terahash – Lower is Better)

Data source: Real operator benchmarks April 2026. Electricity still dominates 60-80% of costs. The newer the hardware and the cheaper the power, the more you keep. I love tariffs when they protect American miners forging real wealth in a free market.

FREE DOWNLOAD: My 7-Pathways to Financial Prosperity (includes exact Bitcoin mining energy strategy framework)

GET THE PDF →The Discipline Tax Visualized

Comfort masquerading as “balance” kills miners faster than any bear market. The charts above don’t lie: the guys running 4¢ power and newest ASICs are still printing while the “I’ll upgrade later” crowd are shutting machines. I still wake at 4:30 a.m. to review hash rate, power contracts, and uptime—because systems beat hype every single time.

Cheap power + iron will is the ultimate free-market cheat code. The next cycle belongs to those who paid the discipline tax early.

Stories and advice from Jaxon Forge, Founder of MoneyForged.com • @MoneyForgedHQ on X • Huge supporter of capitalism and free markets. Love tariffs when they level the playing field.

Ready to turn cheap power + iron discipline into your next wealth engine?

Join 47,000+ builders getting the weekly dispatch on systems, discipline, and boring businesses that actually print money.

SUBSCRIBE FREE – START FORGING TODAY