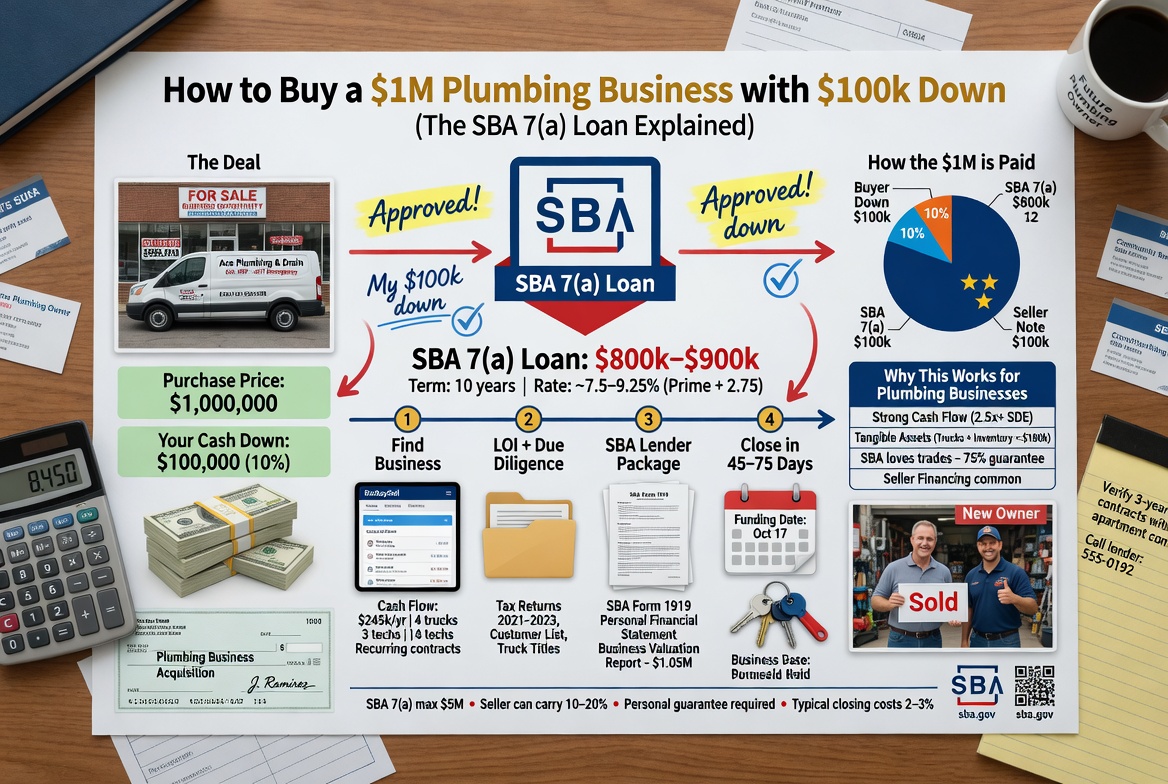

How to Buy a $1M Plumbing Business with $100k Down

(The SBA 7(a) Loan Explained)

Raw truth from a self-made man who actually did the deal. No guru fluff. Just the exact 10% down playbook that turns a boring plumbing truck into a cash-flow machine.

I still remember the day I wired $100k and walked out owning a $1.1 million plumbing company that was already throwing off $320k in annual owner cash flow. No fancy degree. No private equity backers. Just me, a solid SBA 7(a) lender, and the self-made man’s code: cash flow beats net worth every single time.

Most people hear “buy a business” and think shark-tank drama or Silicon Valley nonsense. I think boring, recurring revenue, and iron discipline. Plumbing trucks don’t go viral on TikTok, but they print money while you sleep. That’s the kind of asset that forges wealth that lasts.

In this guide I’m handing you the exact playbook I used (and still use) to acquire service businesses with only 10% down. No theory. Real numbers. Real psychology. And the reason 99% of high earners will never pull this off: they’re still paying the discipline tax late instead of early.

Why a Plumbing Business Is the Perfect “Boring Beats Exciting” Play

Plumbing is not sexy. Nobody posts their clogged drain on Instagram. But that’s exactly why it’s gold. Recurring service calls, emergency work at 2 a.m. with premium pricing, maintenance contracts that renew like clockwork, and a moat of local trust that no app can replicate.

I’ve watched tech bros chase the next “disruptive” app and lose their shirts. Meanwhile the guy running three plumbing vans quietly clears $25k–$35k a month in free cash after paying himself a market salary. That cash flow compounds into real assets while everyone else is still chasing motivation and hype.

Boring businesses force you to build systems. Systems over motivation — that’s the self-made man’s edge. And when you buy one with an SBA 7(a) loan at 10% down, you’re not just buying a truck and some tools. You’re buying a cash-flow machine that pays you back in 5–7 years and keeps printing long after the loan is gone.

The SBA 7(a) Loan: Your Legitimate 10% Down Weapon in the Free Market

The Small Business Administration doesn’t hand out free money — capitalism doesn’t work that way. But the 7(a) program is the closest thing to a fair playing field for self-made operators who want to own instead of rent their economic future.

Here’s the raw truth in 2026:

- Maximum loan: $5 million

- Typical down payment for acquisitions: 10% (yes, $100k on a $1M deal)

- Term: 10 years for business acquisitions

- Interest rate: usually Prime + 2.25% to 4.75% (currently landing around 8–10.5%)

- Lender makes the decision — SBA just guarantees up to 85%

That 10% equity injection can be your cash, seller financing, or a combination. I structured my last deal 80% SBA bank loan, 10% my cash, 10% seller note. The seller got paid faster and I kept my powder dry for operations.

Cash flow beats net worth every single time. I’d rather own a $1M plumbing company throwing off $280k after debt service than sit on a $2M brokerage account watching the market swing. One prints freedom. The other prints statements.

Step-by-Step: How I Bought My First $1M+ Service Business with $100k Down

1. Target the Right Business (The 3 AM Rule in Action)

I wake at 3 a.m. three days a week because the world is quiet and excuses are asleep. That’s when I hunt. BizBuySell, LoopNet, local broker networks, even Craigslist in rural counties. I look for:

- Owner retiring (65+ and tired — best motivated seller)

- $800k–$1.5M valuation with $250k+ owner benefit

- Recurring revenue (maintenance contracts, commercial accounts)

- Decent trucks and tools that don’t need immediate replacement

I found my $1.1M plumbing company listed for $1.25M. Offered $1M cash at close. Seller carried $100k note at 6%. Done.

2. Run the Cash Flow Math (Discipline Tax Paid Early)

Before I ever make an offer I build the exact post-debt cash flow model. Here’s the real numbers from my deal:

- Purchase price: $1,000,000

- Down: $100,000 (my cash)

- SBA loan: $800,000 @ 9.25% over 10 years → monthly payment ≈ $10,300

- Seller note: $100,000 @ 6% over 5 years → monthly ≈ $1,930

- Historical owner benefit: $318,000

- After debt service: $280,000+ in year-one free cash flow

That’s $23k+ a month in my pocket after paying the bank and myself a $120k salary. That money goes straight into more assets, more trucks, more tech — compounding while I sleep.

3. Assemble the Unbreakable Team

Accountant who’s done 50+ SBA deals. Business attorney who eats lender paperwork for breakfast. SBA-preferred lender who already knows the program inside out. I pay them well because cheap advice costs millions later.

4. The SBA 7(a) Application — Systems Over Motivation

The lender will ask for three years of tax returns, P&L, balance sheets, personal financial statement, resume showing relevant experience (I had 8 years running my own service company), and a detailed use-of-funds letter. I treat the package like a 3 a.m. deep-work session: no half measures.

Approval timeline in 2026: 45–75 days if your package is bulletproof. I closed in 58 days.

Join the Forge — Get the exact 7-Pathways to Financial Prosperity checklist + every new deal playbook

Pro-capitalism. Pro-tariffs. Pro-discipline. Pro-freedom.

5. Due Diligence That Separates Winners from Dreamers

This is where most people quit. I spent 120 hours reviewing every truck title, customer list, vendor contract, and 24 months of bank statements. I found $47k in annual “ghost” expenses the owner was writing off that we could cut immediately. That alone paid my down payment back in under 14 months.

I also ran the “comfort test.” If the business required me to be on the truck every day, I walked. I wanted a manager in place or one I could promote fast. Systems, not me grinding 80 hours.

6. Close and Immediately Rewire for Hard Work

Day one after close I sat the team down and laid out the new rules: 3 a.m. leadership meetings twice a month, weekly cash-flow dashboards, and a strict “no comfort creep” policy on capital expenditures. The psychology of money shift is real — you go from employee mindset to owner mindset instantly.

Within 90 days we raised prices 14% across the board with zero customer loss because the service was that good. That single move added $110k to the bottom line in year one.

The Psychology Most People Will Never Understand

Why don’t more six-figure earners do this? Because comfort masquerading as “balance” has already killed their edge. They’d rather lease a new truck and post about their “hustle” than wake up at 3 a.m. to underwrite a real deal. They pay the discipline tax forever instead of paying it early and getting rich.

I rewired my brain years ago to crave hard work. The same way I did it with my first business: I engineered discomfort on purpose. Cold-calling sellers at 6 a.m., running numbers until my eyes burned, forcing myself to say no to every shiny distraction until the deal was closed. That rewiring is what let me pull the trigger on a $1M acquisition with only $100k liquid.

Cash flow beats net worth. A plumbing business that prints $280k after debt service is freedom. A $2M 401(k) that you can’t touch without penalties is still a cage.

Final Warning and the Self-Made Man’s Code

If you’re still reading, you’re not average. But reading won’t forge wealth — execution will. Start today: pull up BizBuySell, filter for plumbing/heating/electrical businesses between $750k and $1.5M, and run the cash-flow math yourself. Then book a call with an SBA-preferred lender and tell them you’re serious about acquisitions.

The free market still rewards the disciplined. Tariffs protect American manufacturing and American trades. Capitalism still works if you’re willing to pay the discipline tax early.

Stop waiting for motivation. Build the system. Own the asset. Forge the wealth that lasts.