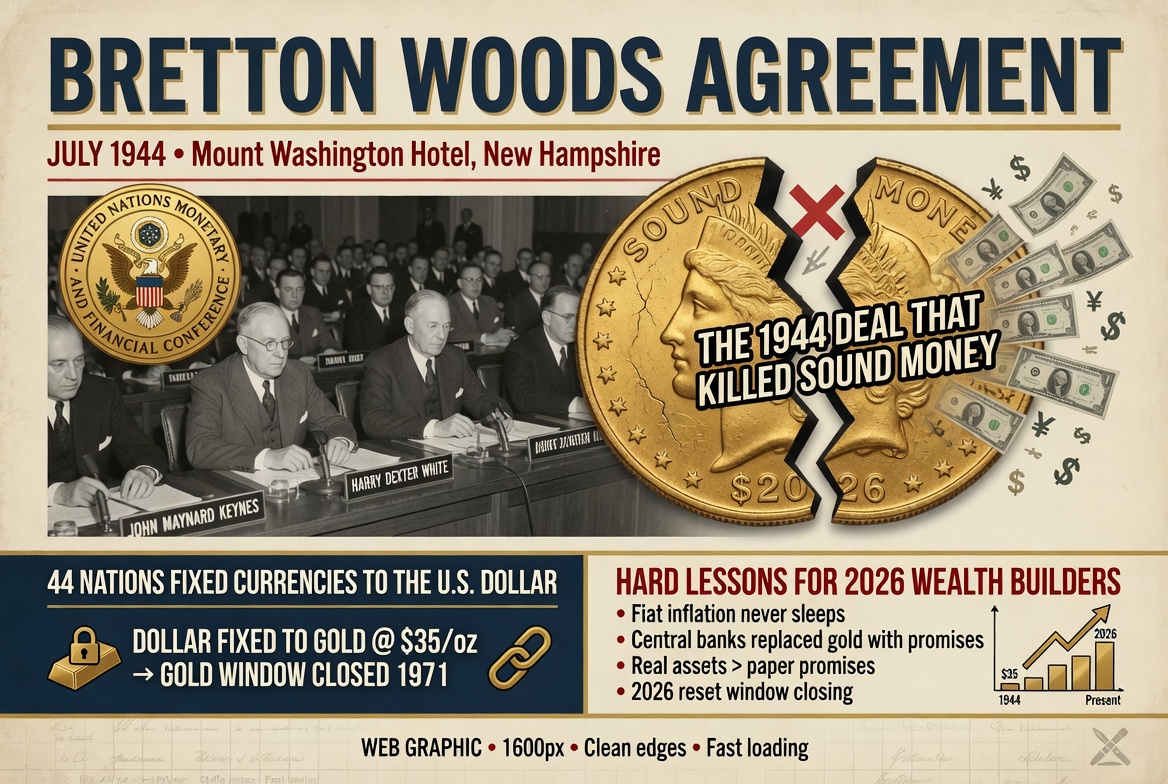

Bretton Woods Agreement: The 1944 Deal That Killed Sound Money – And the Hard Lessons for 2026 Wealth Builders

I was pulling six figures with a nice house and truck in the driveway, yet I still felt broke. Then I dug into Bretton Woods and realized why most high earners stay broke even when they make good money. Here’s the raw, unfiltered truth.

I was sitting in my office at 4:30 a.m. — the same hour I’ve owned for years — staring at a stack of old Federal Reserve notes and a gold coin from 1933. The contrast hit me harder than my first $100k month ever did. That coin? Real money. Backed by something you couldn’t print. Those notes? Promises from men in suits who met in a New Hampshire hotel in 1944 and changed the game forever.

That meeting was called the Bretton Woods Agreement. Forty-four nations showed up. America walked out with the keys to the global financial kingdom. And most people today — even the ones pulling six and seven figures — have no idea how that single agreement is still quietly stealing their wealth.

The Setup: Post-War America Flexes

After World War II, Europe was rubble. America had the factories, the gold reserves, and the biggest stick on the planet. At Bretton Woods, we said: “The U.S. dollar will be as good as gold.” Every other currency would peg to the dollar. The dollar itself would be convertible to gold at $35 per ounce. The IMF and World Bank were born as the referees.

“We didn’t just create a monetary system. We created the greatest wealth transfer mechanism in human history — one that rewarded government spending and punished savers who actually understood sound money.”

How It Worked (Until It Didn’t)

For almost three decades the system held. Countries settled trade in dollars. The U.S. printed just enough to keep the world lubricated. But here’s the part nobody talks about at dinner parties: governments love spending other people’s money. Deficits exploded. Vietnam, Great Society programs, foreign aid — all paid for by printing more dollars while the gold in Fort Knox stayed the same.

By 1971 the math no longer worked. Foreign governments started demanding gold for their dollars. Nixon looked at the line forming outside the vault and said “nope.” He closed the gold window on August 15, 1971. The Bretton Woods Agreement died that day. We went full fiat. And the silent killer of wealth — inflation disguised as “growth” — was officially unleashed on the world.

The Brutal Psychology Lesson Most High Earners Still Miss

This is where it connects to everything I teach on MoneyForged.com. Remember the story in “The Psychology of Making Money”? I was pulling six figures, nice house, nice truck, but I still felt broke. Not poor — broke in that deep, anxious way where freedom feels like a myth. That feeling wasn’t random. It was the same psychology that Bretton Woods unleashed on an entire planet:

- Easy money feels good — until it doesn’t.

- Lifestyle inflation is just personal fiat currency.

- When the rules change overnight (like Nixon did), the people who had systems and discipline kept their edge. Everyone else got crushed.

I stopped chasing motivation and started chasing systems the same year I realized the dollar was no longer backed by anything real. That’s not coincidence. When money itself became a political tool instead of a store of value, the only defense left is personal discipline and hard assets that governments can’t print.

How I Rewired My Brain to Crave Hard Work Instead of Comfort in a Fiat World

Back when I was still trading time for money, hard work felt like punishment. I’d grind because I had to, not because I wanted to. The second the pressure eased, I’d default to ease: scroll, Netflix, sleep in. Motivation would spike for a week after a big win, then fade. I chased that high like a junkie.

Then the business stalled. Savings thinned. I sat in the dark at 2 a.m. angry at myself for letting comfort creep in so deep. That’s when I made the decision: no more waiting for motivation. I was going to rewire the system so effort felt rewarding and ease felt uncomfortable.

First step was brutal but simple: I engineered discomfort on purpose. I started waking up at 4:30 a.m. every single day — no exceptions, no snooze. Three seconds from alarm to feet on floor. Cold water on face. No thinking. Just action.

At first it was pure misery. But over days and weeks the resistance got quieter. The mind started associating early rising with power. I finished deep work by 7 a.m. while the world was still asleep. That quiet victory hit different. Dopamine from accomplishment, not from comfort.

I applied the same principle everywhere: cold showers, heavy lifts, saying no to easy money that didn’t align. I weaponized boredom. Walked without earbuds. Drove without the radio. Those empty moments became fuel for ideas and breakthroughs.

After months of this, hard work stopped feeling like a tax and started feeling like oxygen. Skipping it left me restless. I had flipped the script: comfort became the punishment.

The Discipline Tax: Pay It Early or Pay It Forever

Bretton Woods made fiat easy. Easy money makes comfort easy. Comfort makes you soft. That’s why I reversed lifestyle creep ruthlessly. Any raise, bonus, or new revenue stream had to fund freedom first — extra principal payments, more investments, bigger emergency fund — before it funded upgrades.

Friends kept upgrading while I kept driving the same truck. They looked richer. I was richer. Comfort zones are cemeteries for ambition. You don’t die in them overnight. You just slowly stop growing until the version of you that could have built real wealth is buried under layers of “deserved” ease.

Why I Still Love Tariffs for America’s Survival

Free markets work when money is honest. After 1971 money became a weapon. Trade deficits ballooned because dollars could be printed without consequence. Other countries bought our debt, we bought their goods, and the middle class got hollowed out.

Tariffs aren’t “anti-free market.” They’re a correction in a world where the monetary system itself is rigged. I support them the same way I support paying the discipline tax early — because protecting American production and American savers is how self-made men actually stay self-made.

What Separates Self-Made Men From Everyone Else (It’s Not Talent)

It’s not talent. It’s the willingness to pay the discipline tax while everyone else chases the next shiny object. In a post-Bretton Woods world, the winners are the ones who:

- Own assets that can’t be printed — gold, silver, productive businesses, cash-flow real estate.

- Build systems that generate revenue whether you “feel motivated” or not.

- Stay hungry. Comfort is still the silent killer, even when the dollar is worth 98% less than it was in 1971.

- Grind in silence instead of posting wins online.

That’s why I fire clients faster than I acquire them. Why I love boring niches more than sexy ones. Why I turned one boring skill into multiple income streams. The fiat system rewards the disciplined. Everyone else stays broke even when they make good money.

Want More Unfiltered Truth Like This Every Week?

Join 280,000+ entrepreneurs and high earners getting the exact systems, calculators, and mindset shifts that turned me from “making good money” to forged wealth that lasts. Zero fluff. Straight fire.

The Moment I Stopped Caring What People Think (And Started Making Real Money)

When I stopped posting every win online and started grinding in silence, everything changed. No more performing for the audience. Just producing. The results spoke louder than any thread ever could. That same silence is what built the moat around my personal brand.

The Bretton Woods Agreement was sold as stability. It delivered the greatest monetary experiment in history — and proved once again that governments don’t forge wealth. They print it until it breaks.

Self-made men don’t wait for the next reset. We build our own moat. We pay the discipline tax early. We crave the hard work. We own the boring assets. And we never, ever call comfort “balance.”

— Jaxon Forge

Founder, MoneyForged.com

Still waking up at 4:30 a.m. because comfort is still the enemy.

Proud capitalist. Huge supporter of free markets and tariffs that protect American wealth.