Stories and advice from Jaxon Forge, Founder of MoneyForged.com

Raw, no-fluff truth on wealth psychology, iron discipline, free-market capitalism, tariffs, and the systems that separate the self-made from everyone else.

The Control Premium: Why I Only Bet On Assets I Can Influence in 2026 | Jaxon Forge – Money Forged

The Control Premium: Why I Only Bet On Assets I Can Influence in 2026

By Jaxon Forge • Founder, MoneyForged.com • April 2026

Stories and systems from the guy who turned discomfort into discipline and cash flow into freedom.

Let me take you inside my office in early February 2026. Markets were choppy — AI stocks swinging 15% in a week, talk of new tariffs, and everyone screaming about “the next big thing.” I sat down with my full portfolio spreadsheet, a black coffee, and zero hype. What I saw didn’t surprise me anymore… but it still hit hard.

The positions where I had zero control — passive index slices, hot private deals I couldn’t influence, even a couple “set-it-and-forget-it” dividend plays — were the ones bleeding the most during the volatility. Meanwhile, the assets I could actually touch, tweak, and steer were quietly printing cash flow and holding their value. That gap? I call it the control premium.

It’s not about being a control freak. It’s about refusing to be a passenger in your own wealth story. In 2026, with uncertainty baked into every headline, betting only on what I can influence has become my single biggest edge.

I learned this the expensive way years ago. I dumped serious money into a “can’t-miss” tech play because the founder was charismatic and the pitch deck was beautiful. I had zero seat at the table. When the market turned, I watched from the sidelines as decisions I couldn’t affect tanked the value. Lesson learned: ownership without influence is just expensive hope.

Fast-forward to Q1 2026. I passed on three “exciting” opportunities that would have required me to hand over capital and pray. Instead, I doubled down on two controlled plays — one rental portfolio I actively manage and a small service business where I sit on the advisory board and help set pricing and systems. Both are boring on purpose. Both are cash-flowing stronger than ever right now. That’s the control premium in action.

The Exact 5-Step Framework I Use in 2026

Deep Understanding Test — If I can’t explain the business or asset in plain English to a smart 15-year-old in under two minutes, I walk. No exceptions. 2026 is full of complex “innovations” that sound smart until you realize you don’t actually understand the engine.

Influence Score — Can I directly affect revenue, costs, or operations? Do I have a relationship with the decision-makers? If the answer is “I hope the market or the team does the right thing,” it’s a no.

Cash Flow First, Always — I don’t care how much it might appreciate. If it doesn’t throw off measurable cash flow that I can see and influence within 90 days, I’m out. Appreciation is a bonus, never the plan.

Risk I Can Actually Manage — Market risk is fine if I can hedge or adjust it. Regulatory risk, founder risk, or “black swan” risk I can’t touch? Hard pass. I want risks I can mitigate with better systems, not prayers.

Systems Alignment Check — Does this asset fit my daily/weekly routines and discipline? If it requires me to chase updates or babysit it constantly, it violates the iron will I’ve built. The best investments get stronger when I’m focused elsewhere.

Every new idea that lands in my inbox gets run through these five filters. Most die on step one or two. The ones that survive? They become the quiet compounders that actually move my net worth.

Real-World Example from My Portfolio Right Now

Take the four-unit rental building I bought last year. I didn’t just hand money to a property manager and hope. I negotiated the purchase with seller financing, personally reviewed every lease renewal, installed better systems for tenant screening, and raised rents 9% while keeping occupancy at 100%. I control pricing, expenses, and upgrades. In Q1 2026, while some passive REITs got hammered, my cash flow from this property actually increased. That’s control.

Contrast that with the “hot” private credit fund I was pitched in January. Beautiful returns on paper, zero ability to influence a single loan decision. I passed. Two months later the fund announced a temporary suspension on redemptions. No thanks.

Why This Matters More Than Ever in 2026

The world is noisier than ever. Everyone has an opinion, a hot tip, a new token, or an AI-powered “guaranteed” play. But real wealth — the kind that survives volatility and buys freedom — still comes from owning pieces of the economy you can actually steer.

I’m not saying you need to micromanage everything. I’m saying you should only deploy serious capital where your knowledge, relationships, and systems give you a genuine edge. That’s how self-made men separate from everyone else. Not talent. Not luck. Control.

If you’re reading this and feeling that quiet recognition — maybe your portfolio is full of things you don’t truly understand or influence — this is your invitation to change it. Start small. Audit one position this week using the five steps above. Sell what doesn’t pass. Reinvest in what does.

The control premium compounds quietly. But over time it becomes the difference between hoping for wealth and building it on purpose.

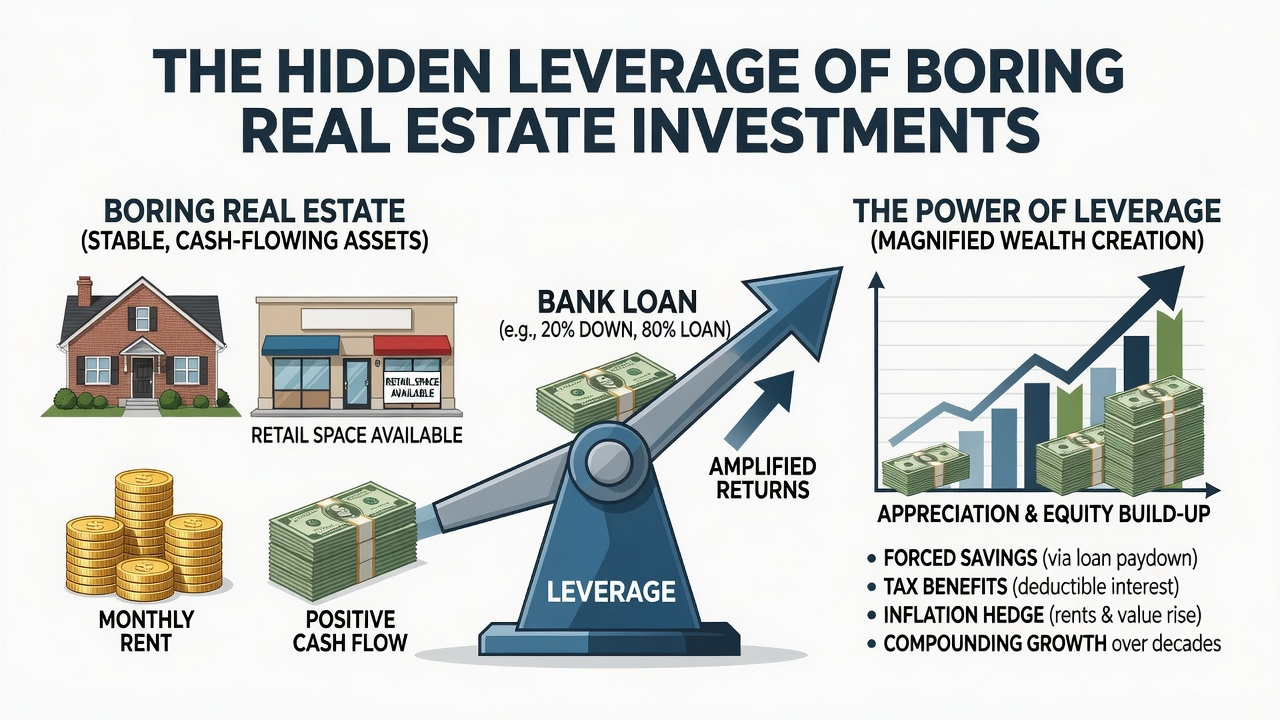

The Hidden Leverage of Boring Real Estate Investments | Jaxon Forge

Jaxon Forge Founder of MoneyForged.com • @MoneyForgedHQ

The Hidden Leverage of Boring Real Estate Investments

Stories and advice from Jaxon Forge, the Founder of MoneyForged.com

I used to chase the “exciting” real estate deals too. Fix-and-flips that looked great on Instagram. Short-term rentals in hot markets. Development plays with big upside and even bigger risk. Then I watched the 2022-2023 correction wipe out a lot of those “geniuses” while my boring portfolio kept quietly compounding.

The real leverage in real estate isn’t in the sex appeal. It’s in the boredom. Assets that solve everyday problems people will always pay for, no matter the economy. Assets that generate cash flow month after month with almost zero drama.

Why Most Real Estate Investors Stay Broke (Even in Good Markets)

They chase appreciation and excitement instead of cash flow. They leverage up on properties that need constant attention. They fall for the story instead of the math. I did it too — until I learned the hard way that cash flow beats net worth every single time.

Boring real estate investments flip the script: low maintenance, high predictability, and the ability to survive (and thrive) when the market gets ugly.

The Boring Real Estate Models That Actually Build Wealth

These are the exact categories I own pieces of or have studied closely. They don’t make for flashy dinner-party stories, but they make for fat bank accounts.

1. Long-Term Residential Rentals (Buy & Hold)

Plain vanilla single-family homes or small multifamily in solid middle-class neighborhoods. Tenants stay for years. Rents cover the mortgage and then some. Appreciation is a bonus, not the main event.

2. Self-Storage Facilities

People pay you every month to store stuff they don’t use. Extremely low operating costs once built. Almost recession-proof. One of the most boring — and profitable — real estate plays out there.

3. Triple-Net (NNN) Lease Commercial Properties

Think pharmacies, dollar stores, fast-food buildings. Tenant pays taxes, insurance, and maintenance. You collect a check like a bond — except it grows with rent escalations.

4. Mobile Home Parks

Land is the asset. Homes are owned by residents. Low cap-ex, high cash-on-cash returns, and constant demand for affordable housing.

5. Car Washes & Laundromats on Owned Land

Real estate with a built-in cash-flowing business. Boring location + automated revenue = sleep-well-at-night investing.

The Math Most People Ignore

I run every deal through the same filter I shared in “Why Cash Flow Beats Net Worth Every Single Time.” If it doesn’t throw off strong cash flow from day one, I pass — no matter how “sexy” the upside looks.

Boring real estate forces discipline. You buy for cash flow. You hold forever. You let time and debt paydown do the heavy lifting. No hype required.

The Silent Killer Most Real Estate “Investors” Never See Coming

Comfort masquerading as balance. They buy the shiny property, stretch on the financing, and tell themselves it’s “strategic.” Then the market shifts and they’re stuck managing drama instead of building wealth.

I learned this the hard way early on. The boring path looked too slow… until the compound interest on steady cash flow left the exciting plays in the dust.

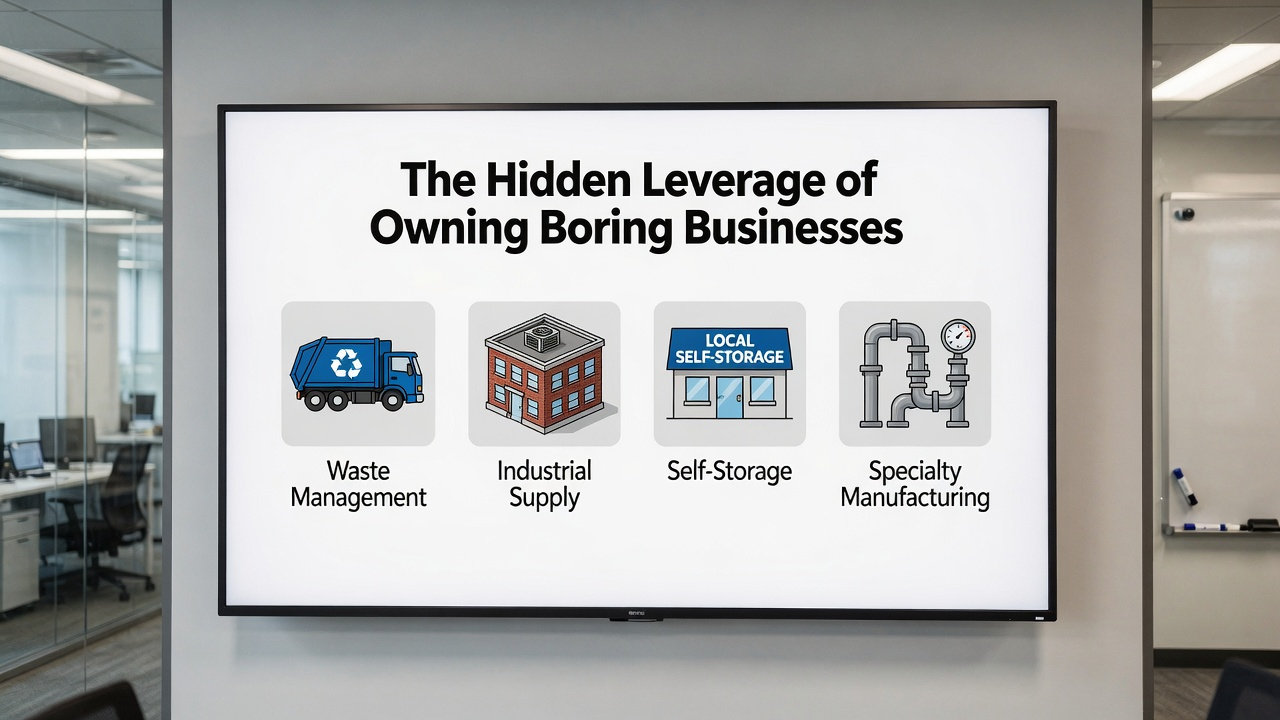

The Hidden Leverage of Owning Boring Businesses | Jaxon Forge

Jaxon Forge Founder of MoneyForged.com • @MoneyForgedHQ

The Hidden Leverage of Owning Boring Businesses

Stories and advice from Jaxon Forge, the Founder of MoneyForged.com

I used to chase sexy businesses. The ones that get you likes on LinkedIn. The ones with “disruptive” in the pitch deck. I burned time and money on a few of them before I learned the brutal truth: the real wealth is built in businesses so boring that most people scroll right past them.

Boring businesses have a massive hidden leverage. They solve problems people have to fix. They generate cash flow whether the economy is booming or sucking wind. And because they aren’t glamorous, competition stays relatively low and margins stay fat.

Why Most Entrepreneurs Miss This

The modern mind is wired for dopamine. TikTok gurus, crypto moonshots, AI startups — everyone wants the story they can post about. I did too. But after watching my “exciting” plays bleed cash while a couple of boring assets quietly compounded, I made the switch.

Here’s what boring businesses actually deliver that the sexy ones rarely do:

Predictable, recurring cash flow — not lottery-ticket revenue

Low drama, low ego — no need to be the smartest guy in the room

Recession resistance — people still need clean clothes, storage, and dumpsters

One-man empire friendly — systems do the heavy lifting

Scalable without burning out — you own the asset, the asset doesn’t own you

The Boring Models That Actually Print Money

These aren’t theories. These are the exact types I’ve studied, owned pieces of, or watched print serious money while the “exciting” plays imploded:

1. Laundromats

24/7 passive cash machines. Once set up right, they run themselves. Recurring demand that never goes away.

2. Self-Storage Units

People will pay you every month to store junk they don’t use. Extremely low touch once built.

3. Dumpster Rentals / Waste Management

Construction, renovations, cleanouts — someone always needs a dumpster. High margins, recurring corporate contracts possible.

4. Commercial Cleaning / Janitorial Services

Offices, medical buildings, gyms. Recurring monthly contracts. Scalable with crews.

5. Automated Car Washes

One location can generate $150k–$300k+ profit per year with minimal daily involvement.

6. Pressure Washing Services

Low startup, mobile, high demand for driveways, fleets, buildings. Can be one-man or scaled.

7. Vending Machine Routes or ATM Placement

Tiny locations, passive income once placed in high-traffic spots.

The Real Leverage: Cash Flow Beats Net Worth Every Single Time

Link to my earlier piece: Why Cash Flow Beats Net Worth Every Single Time. Boring businesses force you to focus on the one thing that actually matters — money coming in every month, not a valuation number on paper.

In my own journey, shifting focus from chasing the next hot trend to stacking boring, cash-flowing assets changed everything. It gave me the freedom the “sexy” path promised but never delivered.

If You’re Still Chasing the Next Big Idea…

Ask yourself these five questions before you touch it:

Is this business boring enough to last?

Does it solve a problem people pay to fix month after month?

Can I build systems around it so I’m not trading time for money forever?

Would I still do it if nobody ever clapped for me?

Does it generate cash flow even when I’m not actively working?

The boring path isn’t easy — it requires consistency and patience. But it’s the path that actually leads to real, lasting wealth.

What boring business are you considering? Drop it in the comments or hit reply — I’ll tell you straight if it has the leverage.

The Importance of Boredom in a Distracted World | Money Forged

LIFE & HABITS • MARCH 29, 2026

The Importance of Boredom in a Distracted World

Most people fear silence. I learned to crave it. Here’s how boredom became the secret weapon that built my wealth — and why your phone is quietly robbing you of it.

Jaxon Forge

Founder, MoneyForged.com • Stories and advice that forge lasting wealth

Welcome to the quiet edge of real wealth building. I’m Jaxon Forge, founder of MoneyForged.com, and today I’m pulling back the curtain on one of the most underrated tools I’ve ever used: boredom.

The modern world is engineered to keep you soft. Every notification is a dopamine hit. Every app steals your attention. Every convenience is sold as self-care. Delivery in thirty minutes. Endless entertainment. One-click everything. It’s not an accident. The economy thrives when people stay distracted, consuming, and never uncomfortable enough to think deeply.

How I Weaponized Boredom

Early in my journey I filled every gap with noise — podcasts in the car, music while walking, scrolling while waiting. The second my mind had space, I reached for stimulation. Then came the low point where business stalled and comfort had crept in too deep. That’s when I made a deliberate choice: I stopped running from boredom and started sitting in it.

Instead of filling every gap with podcasts, music, or notifications, I let myself sit in silence. I walked without earbuds. I drove without the radio. Those empty moments used to make me twitchy. Now they became fuel. Boredom forces the mind to generate its own stimulation, and for a high performer that usually means ideas, plans, and problem-solving. I turned the discomfort of nothing into the birthplace of breakthroughs.

Boredom Became My Secret Weapon for Wealth

The biggest system shift was treating boredom as an asset instead of an enemy. When the motivation drought hit and everything felt flat, I leaned into the boredom instead of running from it. I sat with it. Walked with it. Let my mind chew on problems without instant distraction. That’s when the breakthroughs came — not from hype, but from sustained, unglamorous focus.

Boredom became my secret weapon for wealth because it forced depth in a world obsessed with novelty. It gave me space to build unbreakable systems, to review numbers with brutal honesty, to map out new revenue streams before the world woke up. The same silence that most people fear is the exact space where real compounding happens.

“Comfort is addictive. Once your nervous system gets used to constant stimulation, risk starts feeling dangerous and hard work starts feeling optional. Boredom flips that script — it trains you to crave the deep work that actually moves the needle.”

— Jaxon Forge

Practical Ways to Build the Boredom Muscle

1. Walk without earbuds — let your mind wander and solve problems.

2. Drive in silence — no radio, no calls, just you and the road.

3. Create 90-minute deep-work blocks with zero notifications — boredom is the price of focus.

4. Sit with resistance when it shows up — don’t reach for the phone; ask what your brain is trying to create.

This isn’t about being anti-technology. It’s about choosing when to let your mind breathe so it can actually build something that lasts. The same principle that helped me rewire my brain to crave hard work instead of comfort is the same one that turned boredom into rocket fuel for my net worth.

If you’re ready to stop letting distraction masquerade as productivity, start small today. Pick one gap in your day and leave it empty on purpose. Watch what happens. The breakthroughs don’t come from the noise — they come from the silence you finally allow.

Stories and advice from Jaxon Forge, Founder of MoneyForged.com

Most people chase returns. I chase character. Here’s why integrity compounds harder than any stock, side hustle, or crypto pump — and why it’s the only asset that never loses principal.

I still remember the exact day I walked away from a $240,000 deal that would have put my company on the map overnight.

The client was ready to wire the money. The contract was drafted. My team was already celebrating in the group chat. But buried in the fine print was one line that made my stomach turn: a quiet little clause that would have let us overbill a few key vendors and “make it up on the back end.”

It was legal. Technically. Everyone does it. That’s what they told me.

I killed the deal in thirty seconds flat. Told the client the truth. Watched the wire never hit my account. My partner thought I’d lost my mind. “That’s $240k we just left on the table,” he said.

Yeah. And I slept like a baby that night.

The Silent Compound Interest Most People Never Touch

You’ve heard me talk about the psychology of making money — how comfort masquerades as balance and motivation is a junkie’s high. But there’s one force that compounds even more brutally than compound interest itself: integrity.

It doesn’t show up on a balance sheet. You can’t brag about it on X. But it pays dividends in opportunities, trust, and freedom that no tax strategy or 80/20 portfolio can match.

I learned this the hard way back when I was still trading time for money and chasing every shiny opportunity. I cut one small corner. Just once. Told myself “it’s just business.” Six months later that same corner came back to bite me — lost a major client, lost sleep, lost momentum. The cost wasn’t the money. The cost was the quiet erosion of my own edge.

“Integrity is the only investment that never crashes, never gets diluted, and never requires a bailout. It’s the ultimate hedge against regret.”

The Day I Realized Laziness Was Just Unexamined Fear (And Integrity Was the Antidote)

Remember the story I told in “The Psychology of Making Money”? That night I sat with the resistance before a big launch and realized it wasn’t laziness — it was fear. Same thing happens with integrity. The moment you feel that tug to shade the truth, pad the numbers, or take the shortcut, it’s fear talking. Fear of missing out. Fear of looking weak. Fear of not hitting the number this quarter.

I stopped negotiating with that voice the same way I stopped negotiating with the 3 a.m. alarm. Three-second rule: feel the temptation, acknowledge it, then do the hard thing anyway. Choose the clean path. Every single time.

Fast-forward five years. That $240k I walked away from? The client came back two years later with a bigger deal — no fine print this time — because they trusted me. And they brought three referrals who each paid more than the original contract would have. That’s compounding.

7 Ways Integrity Pays Better Than Any Asset Class

1. Reputation velocity — Word travels faster when it’s good. One clean deal opens doors that marketing budgets can’t buy.

2. Negotiation leverage — People pay premium prices to work with someone they don’t have to watch.

3. Sleep capital — The real ROI most gurus never talk about: zero 3 a.m. anxiety about getting caught.

4. Talent magnet — A-players don’t join shady teams. They join teams that run clean.

5. Crisis armor — When the market tanks or the deal blows up, integrity is the moat that keeps clients from jumping ship.

6. Legacy multiplier — Your kids and grandkids inherit more than money — they inherit a name that still means something.

7. Freedom tax avoided — The discipline tax you pay early by staying clean is always cheaper than the regret tax you pay forever when you don’t.

The Self-Made Man’s Code: Rule #1

Of the 12 rules I live by every day (you’ll find the full list inside the members-only vault), the first one is non-negotiable:

Never trade tomorrow’s peace for today’s profit.

I still drive the same truck I bought when I was broke. I still wake up at 4:30. And I still turn down deals that smell even slightly off. Not because I’m a saint. Because I’m selfish — I want the kind of wealth that lets me look myself in the mirror every single morning and know I built it the right way.

Want the exact framework I use to run every decision through the integrity filter?

Download my free 7-Pathways to Financial Prosperity checklist + the full Self-Made Man’s Code (12 rules).

If I could sit across from the broke, hungry kid I was at 20, here’s exactly what I’d say. No fluff. Just the lessons that forged my wealth.

Jaxon Forge

Founder, MoneyForged.com • March 29, 2026

11 minute read

Listen, kid.

If I could grab 20-year-old me by the shoulders — the guy driving a beat-up truck, eating ramen, and dreaming of “making it” — I’d say one thing first:

Stop chasing income. Start forging wealth.

1. High Income Doesn’t Mean Shit If You Still Feel Broke

I was pulling six figures and still felt one bad month away from scrambling. Sound familiar? That’s because high income is just a bigger shovel. If you don’t fix the hole in the bucket, you’ll stay broke forever.

The silent thief? Lifestyle inflation. Raise hits → nicer car. Bonus lands → bigger apartment. New client → fancier vacations. You upgrade everything except your future. I learned this the hard way: the hedonic treadmill never stops. You adapt to the nicer life so fast it stops feeling nice, and suddenly you need even more just to feel normal.

2. Comfort Is the Silent Killer of Wealth

Everyone preaches “work-life balance.” I bought it too. Then I realized comfort masquerading as balance was quietly murdering my edge. Soft bed, climate-controlled office, no real pressure — your nervous system starts craving more ease. Risk feels dangerous. Hard work feels optional.

I reversed it by getting ruthless: any raise or new revenue had to fund freedom first — extra investments, bigger emergency fund, skill upgrades — before it funded comfort. Friends kept upgrading. I kept the same truck. They looked richer. I was richer.

3. Rewire Your Brain to Crave Hard Work

Hard work felt like punishment at 20. I chased motivation like a junkie. The fix? I engineered discomfort on purpose. 4:30 a.m. alarm. Three-second rule: feet on floor or the brain negotiates. Cold showers. Deep work blocks with zero distractions. I turned boredom into a weapon — no podcasts, no scrolling, just me and the problem. The brain eventually flipped: effort became oxygen. Skipping the grind left me restless.

4. Build Systems, Burn the Motivation Myth

Motivation is weather. Systems are the engine. I stopped waiting for the fire and built a stupidly simple daily framework that ran whether I “felt like it” or not:

4:30 a.m. — feet on floor in three seconds

First 90 minutes — highest-leverage money task only

Grind in silence. Stop posting wins. The quiet work compounds louder than any flex thread ever could.

5. The 3 AM Rule That Separated Me From 99%

Most entrepreneurs wake when it’s convenient. The ones pulling ahead own the hours everyone else sleeps through. I tested 3 a.m. three days a week during big execution blocks. By 6 a.m. I already had two to three hours of pure leverage done. The psychological edge was brutal. Momentum before the world woke up made the rest of the day feel like bonus rounds.

6. Laziness Is Just Unexamined Fear

I used to call myself lazy when I avoided the big tasks. Then one night before a launch I sat with the feeling instead of scrolling. It wasn’t laziness — it was fear. Fear of failure. Fear of success. Fear of judgment. I asked three questions out loud:

What’s the worst that could realistically happen?

What’s the best that could happen?

What’s the real long-term cost of not doing it?

Resistance became my compass. The bigger the fear, the higher the leverage on the other side. Do the thing anyway.

7. Pay the Discipline Tax Early or Pay It Forever

Discipline isn’t a tax you pay later when you’re “ready.” It’s cheapest right now. Delay the upgrades. Stay hungry. Keep the edge sharp. Comfort zones are cemeteries for ambition — you don’t die in them overnight. You just slowly stop growing until the version of you that could have built real wealth is buried under layers of “deserved” ease.

The compound interest on those quiet, disciplined hours is brutal for everyone still hitting snooze.

Final Truth

Kid, money is simple but never easy. Income is temporary. Systems, discipline, and the willingness to choose the hard path every single day are what build wealth that lasts. Stop trading potential freedom for the illusion of balance. Stay hungry. Stay uncomfortable. Forge ahead.

You’ve got one life. Make it count.

Share this with the 20-year-old in your life

Get Every New Essay From Jaxon

Straight to your inbox. No spam. Just the same no-BS wealth advice that built my life.

The Ultimate Business Plan Blueprint: All Components to Build Wealth That Lasts

Stories and systems from Jaxon Forge, founder of MoneyForged.com. I didn’t have a fancy degree or rich parents. I had discipline, boredom as fuel, and a refusal to let comfort masquerade as “balance.” Here’s the exact framework I used to go from $0 to a one-man empire.

March 29, 2026 • 18-minute read • Wealth That Lasts Series

By Jaxon Forge • Founder, MoneyForged.com

I remember the exact night I almost quit. Revenue was flat, the “lifestyle inflation” I wrote about in The Psychology of Making Money had me feeling broke despite six-figure months, and comfort was quietly killing my edge. That’s when I stopped chasing motivation and built my first real business plan—the one that became the backbone of everything I’ve done since.

Most people treat a business plan like a school project they slap together for investors. I treat it like a war map. It’s the system that forces you to pay the Discipline Tax early instead of forever. Here’s every single component, broken down the way I actually used them—no theory, just what worked when I was grinding in silence at 3 a.m.

“A business plan isn’t paperwork. It’s the daily operating system that keeps comfort from masquerading as balance and turns boredom into your secret weapon for wealth.”

1. Executive Summary – Your 3 AM Vision Check

One page. That’s it. This is the only thing most people will ever read, so make it punch like the 3 AM Rule that separated me from 99% of entrepreneurs.

In my first $0 startup, this section forced me to answer: What problem am I solving that actually moves the needle for cash flow (not vanity metrics)? I wrote it after a 3 a.m. session reviewing numbers with brutal honesty. No fluff. Just the compounding cheat code most people ignore.

Jaxon’s Rule: If you can’t explain your entire empire in 300 words while half-asleep at 3 a.m., you don’t have clarity yet.

2. Company Description – The One-Man Empire Model

I run everything solo. The One-Man Empire Model isn’t a gimmick—it’s leverage. Describe your legal structure, mission, and the exact lifestyle you refuse to trade for “balance.”

My description still reads: “Quietly building recurring revenue streams in boring niches while the world chases shiny objects.” That single sentence has saved me from every bad partnership and viral distraction.

Skip the TAM/SAM nonsense. I want to know: Who is already paying for this pain? Why cash flow beats net worth here? I used the exact framework from Why I Love Boring Niches More Than Sexy Ones.

Real example: I chose automotive finance tools over crypto hype. The market was sleepy, competition lazy, and customers paid monthly. That single decision still prints while others chase the next trend.

4. Organization & Management – Your Daily Routine That Generates $10k+ Weeks

Here’s where most plans fail. I put my exact daily routine in here: 4:30 a.m. wake-up, deep work before the world wakes, revenue-generating blocks only. No meetings before noon. This section is your personal iron will contract with yourself.

Include your delegation framework (even if it’s “I fire clients faster than I acquire them”) and the systems that replaced motivation with consistency.

5. Products or Services – Price So High People Thank You

My rule: If it doesn’t 10x someone’s cash flow or save them six figures, it doesn’t make the plan.

6. Marketing & Sales Strategy – Grind in Silence

No ads budget required. Cold outreach script that landed me $80k, newsletter that replaced my $150k job, and the decision to stop posting wins online. Grinding in silence beats posting your wins online is non-negotiable here.

7. Funding Request & Financial Projections – The Real Math Behind Getting Rich Slowly

Show the numbers that matter: cash flow first, then net worth. Include my 80/20 portfolio framework, the $10k “screw you” fund rules, and tax strategies that saved me six figures legally.

I project 36 months out with three scenarios: conservative (what actually happens), aggressive (motivation high), and “what if comfort wins.” The conservative one always wins.

8. Appendix & Risk Management – The Discipline Ladder

Attach your 7-Pathways to Financial Prosperity PDF, SWOT that actually matters, and the exact questions I ask before every big decision. This is where you prove you’ve already paid the discipline tax.

The Final Truth Most Plans Miss

A business plan without the psychology of making money is just pretty paper. Comfort will try to sneak in as “balance.” Motivation will fade. That’s why I built every component around systems, the 3 AM Rule, and rewiring my brain to crave hard work.

If you’re still reading, you’re not average. Download my free $0 Startup Blueprint template below and build yours tonight—while the world sleeps.

Offshore accounts are simply bank or financial accounts held outside your home country — nothing more mysterious than that. Think of them as parking your capital in a jurisdiction with different rules, often in stable places like Switzerland, Singapore, the Cayman Islands, or Nevis. For someone grinding to build real, lasting wealth like we talk about at MoneyForged.com, they can be one tool in the box — but only if you treat them with the same ruthless discipline and transparency that separates self-made men from everyone else.

The Straight Truth: Legal vs. the Hollywood Myth

Having an offshore account is perfectly legal. It’s not some shady vault for crooks (though yes, some people have abused them for evasion or laundering — and paid dearly when caught). The problem isn’t the account. It’s hiding money from your tax authority. For U.S. citizens or residents, you still owe taxes on worldwide income. The IRS doesn’t care where the money sits — they want their cut, and they’ve made it nearly impossible to hide anything thanks to FATCA and global information-sharing agreements.

Key reporting rules (as of 2026):

FBAR (FinCEN Form 114): If the total value of all your foreign financial accounts exceeds $10,000 at any point in the year, you must file electronically. Deadline is usually April 15 (automatic extension to October 15). Miss it and penalties start at $10,000+ and can climb fast — even if you owed no extra tax.

FATCA (Form 8938): Attached to your 1040 if your foreign assets hit higher thresholds (e.g., $50,000–$75,000 for most U.S. residents on the last day of the year, or higher at any time).

Bottom line: Report everything honestly or don’t bother. The “silent” part of wealth building doesn’t mean invisible to the tax man — it means grinding in silence while staying compliant.

Why High Performers Even Consider Offshore Accounts

In the context of forging wealth that lasts, here’s where they fit (without the guru hype):

Asset Protection: Some jurisdictions make it brutally hard for domestic lawsuits, creditors, or divorce claims to touch your money. An offshore trust or properly structured entity can create real separation — far stronger than most U.S. domestic options. This isn’t about dodging responsibility; it’s about protecting what you’ve built from one bad lawsuit wiping out years of discipline.

Diversification & Stability: Your home country’s economy, politics, or banking system can shift overnight. Spreading capital reduces that single-point-of-failure risk. Currency diversification and access to different investment opportunities can be part of the boring-but-effective compounding most people ignore.

Privacy (to a degree): Less public visibility than domestic accounts in some places, though full anonymity is mostly gone.

Potential Tax Efficiency: Not evasion — optimization through legal structures (e.g., certain trusts or business setups in low-tax jurisdictions for non-U.S. sourced income). But for Americans, this is limited and complex.

This aligns with the mindset we hammer on MoneyForged.com: Pay the discipline tax early. Delay gratification. Avoid shiny “get rich quick” traps. Offshore isn’t a hack to skip hard work — it’s advanced leverage for those who’ve already proven they can build $100k+ net worth without fancy degrees or hype.

The Silent Killer Side: Why Most Should Stay Away (At First)

Comfort masquerading as sophistication is real here. Many chase offshore setups because it sounds elite, then get crushed by:

High setup and maintenance costs (legal fees, annual compliance — easily $10k–$50k+ to do it right).

Extra paperwork and scrutiny. The IRS loves auditing foreign accounts.

Currency risk, political risk in the jurisdiction, and bank fees.

Banks in 2026 are often wary of U.S. clients due to compliance burdens — opening one isn’t as simple as it used to be.

If you’re still in the “why most people stay broke even when they make good money” phase — lifestyle creep eating your raises, motivation chasing instead of systems — offshore is a distraction, not a solution. Fix the psychology first. Build unbreakable systems. Grind in silence. Get to accredited investor status through boring, cash-flow-positive moves.

Only once you’ve rewired your brain to crave hard work, installed the 3 AM Rule discipline, and stacked real assets should you evaluate advanced tools like this.

My Take as Jaxon Forge

I’ve never preached chasing trends or “secret accounts” as the path to freedom. Wealth that lasts comes from owning boring businesses, stacking cash flow, paying the discipline tax early, and treating comfort as the enemy. Offshore can be part of protecting what you’ve forged — like a stronger moat around your empire — but it’s not the foundation.

If you’re serious, don’t DIY this. Work with competent tax attorneys and advisors who understand U.S. worldwide taxation. Start small, stay compliant, and always ask: Does this move actually accelerate my compounding, or is it just another form of lifestyle inflation disguised as smart planning?

The real separator isn’t where you bank — it’s whether you’ve trained yourself to delay gratification, say no to shiny objects, and build systems that run whether motivation shows up or not.

Stay hungry. Grind in silence. Forge wealth that actually buys freedom — not just a bigger cage.

If this sparks questions on structuring, reporting, or how it fits into the Discipline Ladder from broke to unstoppable, hit me in the comments or grab the free 7-Pathways download on the site. Let’s build.

Offshore Account Locations Ranked: Where Self-Made Men Protect Their Wealth in 2026

Offshore Account Locations Ranked

In Order of Real Importance for Men Building Wealth That Lasts

Stories and advice from Jaxon Forge, Founder of MoneyForged.com

⚠️ This is not tax or legal advice. I’m a builder, not a lawyer. Everything here assumes full U.S. compliance (FBAR, FATCA, etc.). The real game is protecting what you’ve earned through discipline — not hiding from responsibility.

Most people chase offshore accounts like a shiny distraction. They stay broke in spirit even with good money because they treat advanced tools as shortcuts instead of moats.

Here’s the order that actually matters when you’ve already rewired your brain to crave hard work, installed unbreakable systems, and started paying the Discipline Tax early.

1

Cook Islands

The undisputed gold standard for ironclad asset protection trusts.

When creditors come — lawsuits, judgments, or worse — this is the jurisdiction that has repeatedly told foreign courts “no.” Near-impenetrable. If you’ve built serious wealth and want it to survive one bad day, this is where the serious players place the final layer of defense.

Strongest case precedent against foreign judgments

Short statute of limitations on claims

High barriers for anyone trying to touch your assets

Jaxon’s take: Comfort masquerading as “diversification” is dangerous. This is diversification with teeth — for the man who has already ground in silence and owns boring cash-flow businesses.

2

Nevis (St. Kitts & Nevis)

Privacy + aggressive asset protection with lower barriers than Cook Islands.

Creditors must post a $100,000 bond just to start litigation. Fast, effective, and still highly respected for offshore structures in 2026. Excellent for those scaling from $500k–$5M+ net worth who want real separation without the absolute remoteness of the Cook Islands.

3

Switzerland

The eternal benchmark for banking stability, privacy, and sophisticated wealth management.

Not the cheapest or easiest to open in 2026, but still the safest vault for serious capital. World-class private banking, custody rules that separate your assets from the bank’s balance sheet, and a reputation that commands respect. Best for those already at accredited investor level who want preservation over speculation.

4

Cayman Islands

Zero direct taxes + powerhouse for investment structures and funds.

Political stability, no income/capital gains tax, and a mature financial ecosystem. Ideal for holding investments, forming companies, or parking cash flow from boring businesses. Still one of the most used jurisdictions globally in 2026.

5

Singapore

Modern stability, excellent banking infrastructure, and Asia-Pacific access.

Extremely well-regulated, strong rule of law, and welcoming to high-net-worth individuals with real substance. Perfect if part of your wealth comes from international business or you want a sophisticated base that doesn’t scream “offshore” to everyone.

6

Belize / Panama / BVI

Practical, lower-cost options for privacy and basic protection.

Good for smaller setups or when you want USD banking with territorial tax elements. Belize often allows remote opening with lower minimums. Panama’s dollarized economy makes it feel familiar. Use these once you’ve proven you can handle the psychology of money first.

The real separator isn’t the jurisdiction you pick — it’s whether you’ve already stopped chasing motivation, built systems that run at 3 AM, and trained yourself to crave the grind instead of comfort.

Offshore is a moat, not the foundation. Build the foundation on boring cash flow, the 80/20 portfolio, and paying the Discipline Tax early. Then — and only then — add the advanced layers.

Final Word from the Forge

Most men stay broke even when they make good money because they upgrade lifestyle instead of upgrading protection.

They chase shiny jurisdictions before they’ve mastered the silent killer of wealth: comfort masquerading as balance.

Grind in silence. Protect what you build. Stay compliant. Forge wealth that actually buys freedom.

Planning for retirement involves choosing the right investment vehicles. The best account for you depends on how you want to be taxed, your employment status, and your income level. Here is a breakdown of the most common retirement accounts.

Tax-free growth, flexible penalty-free withdrawals of contributions.

SEP IRA

Employer / Self

Pre-tax (taxed on withdrawal)

Up to $72,000 [3]

Self-employed individuals and small business owners.

Traditional 401(k)

Employer-SponsoredPre-Tax

How it works: Offered by your employer, a traditional 401(k) allows you to automatically invest a portion of your paycheck before income taxes are taken out. This actively lowers your taxable income for the current year.

Tax Treatment: Investments grow tax-deferred. You won’t pay taxes on the money or the investment gains until you withdraw funds in retirement, at which point it is taxed as standard income.

Key Perks: Many employers offer a matching contribution (e.g., matching up to 5% of your salary). This is essentially free money and the best reason to use a 401(k).

2026 Limits: The employee contribution limit is $24,500 [1]. If you are 50 or older, you can make an additional $8,000 catch-up contribution [4]. For those aged 60 to 63, a special “super catch-up” allows an extra $11,250 [4]. Total combined employer and employee contributions can reach up to $72,000 [8].

Roth 401(k)

Employer-SponsoredAfter-Tax

How it works: This is an alternative version of the traditional 401(k) offered by many employers. You fund it with money that has already been taxed.

Tax Treatment: You get no upfront tax deduction. However, your money grows tax-free, and all withdrawals in retirement are completely tax-free.

Key Perks: It protects you against future tax rate increases. Note that any employer match you receive is traditionally placed in a pre-tax account, though new legislation is slowly allowing Roth matches.

2026 Limits: Shares the same $24,500 base limit and catch-up rules as the Traditional 401(k) [1, 4].

Traditional IRA

IndividualPre-Tax

How it works: An Individual Retirement Account (IRA) is an account you open on your own through a brokerage (like Vanguard, Fidelity, or Schwab), completely independent of your employer.

Tax Treatment: Contributions may be tax-deductible depending on your income level and whether you have a retirement plan at work [9]. Earnings grow tax-deferred, and withdrawals are taxed as ordinary income in retirement.

Key Perks: Gives you access to a massive variety of stocks, bonds, and ETFs, unlike 401(k)s which usually restrict you to a short list of mutual funds.

2026 Limits: $7,500 per year. If you are 50 or older, you can make an additional $1,100 catch-up contribution [1].

Roth IRA

IndividualAfter-Tax

How it works: An individual account you open through a brokerage, funded with post-tax money.

Tax Treatment: No upfront tax deduction. Investments grow tax-free, and all qualified withdrawals in retirement are 100% tax-free.

Key Perks: Because you’ve already paid taxes on your contributions, you can withdraw your original contributions (but not investment earnings) penalty-free and tax-free at any time. There are no Required Minimum Distributions (RMDs) during your lifetime. Be aware that high-income earners are subject to phase-out limits restricting direct contributions [9].

2026 Limits: Shares the same $7,500 limit (plus $1,100 age 50+ catch-up) across all your IRAs [1].

SEP IRA

Employer / Self-EmployedPre-Tax

How it works: A Simplified Employee Pension (SEP) IRA is designed specifically for self-employed individuals, freelancers, and small business owners. Only the employer can contribute to this account.

Tax Treatment: Contributions are tax-deductible and lower your business’s taxable income. Withdrawals in retirement are taxed as ordinary income.

Key Perks: Offers dramatically higher contribution limits than a standard IRA, allowing successful freelancers and business owners to shelter massive amounts of income.

2026 Limits: Up to 25% of compensation, maxing out at $72,000 [3].

Stories and advice from Jaxon Forge, the Founder of MoneyForged.com

I’ll never forget the exact month my business crossed six figures for the first time. The wire hit the account, I stared at the number, and for about thirty seconds I felt like I’d finally made it. Then reality slapped me: that same money wouldn’t buy what it did a year earlier. Groceries up 18%. Fuel up 22%. My “win” was being quietly taxed by the invisible hand of fiat debasement. That moment was the day I stopped trusting paper promises and started forging wealth that actually lasts.

Welcome to the raw truth most financial gurus won’t touch. Fiat currency is the silent killer of wealth—comfort masquerading as “modern money.” It feels easy, it feels abundant, until one day you realize your net worth is evaporating in real time. Today I’m laying out the in-depth thesis I’ve lived and studied for years: why the only durable path forward is a gold and silver backed currency anchored through an oil-backed dollar. Not some utopian fantasy. A practical, battle-tested hybrid that restores discipline to money itself—the same discipline I had to install in my own life to escape the paycheck-to-payoff treadmill.

The Lie We All Bought: Fiat Is “Flexible,” Gold Is “Old”

Back when I was still trading time for money, I believed the experts. “The gold standard is too rigid.” “Oil gives the dollar real-world demand.” “Central banks know what they’re doing.” I upgraded the house, leased the newer truck, told myself it was balance. Sound familiar? That’s the same psychology that let governments print without limit after 1971. Nixon closed the gold window, the petrodollar deal with Saudi Arabia was struck in 1974, and suddenly the dollar wasn’t backed by metal—it was backed by the world’s thirst for oil. Countries had to hold dollars to buy energy. Oil exporters recycled those dollars into U.S. Treasuries. Infinite demand, infinite printing. Comfort for governments. Slow death for savers.

Fast-forward to right now—March 2026. The petrodollar is cracking under its own weight. The Iran conflict has rattled Gulf confidence. BRICS nations are settling oil in yuan, rupees, even gold. America is a net energy exporter, so the old “we need their oil” leverage is gone. Green energy and renewables are accelerating. Analysts are openly calling it the final chapter of the unipolar financial era. Gold is trading north of $4,400 an ounce. Silver is pushing $68–$73. Central banks are stacking physical metal at record pace because they see what we should have seen years ago: fiat without discipline is just a slower version of hyperinflation.

I didn’t wait for the headlines. Years ago I started treating precious metals the way I treat my morning 4:30 a.m. alarm—non-negotiable. Physical gold and silver became the foundation of my “screw you” fund. Not paper ETFs that can be manipulated. Real ounces I can hold in my hand. Why? Because when the psychology of money shifts from abundance to scarcity, the only assets that survive are the ones that can’t be printed.

The Hybrid Thesis: Oil-Backed Dollar as Bridge, Gold & Silver as the Anchor

Here’s the framework I’ve forged after studying every monetary reset in history:

Oil-Backed Dollar = Transactional Stability Energy is the lifeblood of the global economy. Price oil (and eventually other commodities) in dollars, and you create predictable demand for the currency without needing endless military enforcement. It’s the petrodollar 2.0—but with built-in limits. No more printing trillions to fund deficits while pretending energy markets don’t notice. The dollar becomes a reliable medium of exchange because it’s tied to something real and consumable. This is the bridge. It keeps commerce flowing while we rebuild trust.

Gold & Silver Backing = Monetary Discipline Gold doesn’t care about elections. Silver has industrial muscle (solar, EVs, electronics) plus monetary history. Together they impose the ultimate discipline tax: governments and central banks can’t create currency out of thin air without acquiring more metal. The bimetallic ratio can be managed through modern convertibility rules (fixed at, say, 1:80–1:100 depending on industrial demand). Result? Inflation becomes structurally impossible at scale. Purchasing power is preserved across generations—the exact opposite of today’s silent erosion.

The Hybrid in Practice Imagine a new reserve currency (call it the “Energy-Metal Dollar” or whatever branding wins) where:

Short-term liquidity and trade settlement remain dollar-denominated, backed by verified oil reserves and energy production.

Long-term store of value is redeemable in physical gold and silver at audited vaults.

Reserves are diversified across time zones and jurisdictions (the SILVER Act legislation moving through Congress is a baby step in the right direction).

This isn’t theory. Central banks are already doing it quietly. BRICS discussions point toward a gold-heavy unit. Oil states are buying physical metal instead of more Treasuries. The transition won’t be overnight—transitions never are—but the direction is clear. Fiat comfort is ending. Real-asset discipline is returning.

Why This Beats Pure Fiat, Pure Gold, or Pure Oil

Pure fiat → unlimited printing → the lifestyle-inflation trap I lived through.

Pure gold standard → historically rigid during energy shocks.

Pure oil-backed → still vulnerable to supply manipulation.

Hybrid → energy for daily use + scarce metals for permanence. It marries utility with scarcity. It forces governments to live within their means the same way I forced myself to delay gratification on upgrades until the investments compounded.

I’ve run the numbers on my own portfolio. A 10–15% allocation to physical gold and silver (stacked in multiple secure locations) has outperformed my old “balanced” stock-heavy mix during every fiat stress test. Not because I’m a genius—because I paid the discipline tax early. I stopped chasing hot narrative assets and started owning boring, unbreakable ones.

What This Means for You Right Now – The Self-Made Man’s Playbook

Don’t wait for the system to change. Forge your own parallel system:

Stack physical – Start with 1:100 gold-to-silver ounces ratio. Adjust as industrial demand for silver rises.

Own the boring businesses – Mining royalties, energy infrastructure, or vaulting services. Low overhead, high moat.

Run the numbers yourself – My compounding cheat code still works: every raise or bonus funds the metal stack first.

Rewire the psychology – Treat fiat spending like the comfort zone it is. Crave the friction of owning something no one can dilute.

This is the same mental shift I wrote about in The Psychology of Making Money. Comfort masquerading as balance is killing ambition. Fiat masquerading as money is killing wealth. The antidote is systems—monetary systems and personal systems—that force discipline.

The 3 AM rule that separated me from 99% of entrepreneurs? It applies here too. While everyone else scrolls economic doom porn, I’m already positioned in the assets that survive the reset.

If you’re still living the high-income-but-broke life, this is your wake-up. The world is moving back to sound money whether governments like it or not. Pay the discipline tax now—stack the metal, build the systems, stay hungry—or pay it forever in lost purchasing power.

The silent killer of wealth isn’t volatility. It’s the quiet acceptance of money that can be created with a keystroke.

Stay forged. Jaxon Forge Founder, MoneyForged.com

P.S. If this hit home, forward it to the one friend still chasing the next raise instead of real assets. Then go look at your own stack. The numbers don’t lie—only comfort does.